DSNews The homepage of the servicing industry

DSNews The homepage of the servicing industry

Serious delinquencies on credit cards and auto loans rose in Q1 to levels not seen in the first quarter in the last three years, largely due to the oil slump that impacted the economy in energy-sector states such North Dakota, Oklahoma, and Texas, according to TransUnion’s Q1 2016 Industry Insights released Wednesday.

Serious delinquencies on credit cards and auto loans rose in Q1 to levels not seen in the first quarter in the last three years, largely due to the oil slump that impacted the economy in energy-sector states such North Dakota, Oklahoma, and Texas, according to TransUnion’s Q1 2016 Industry Insights released Wednesday.

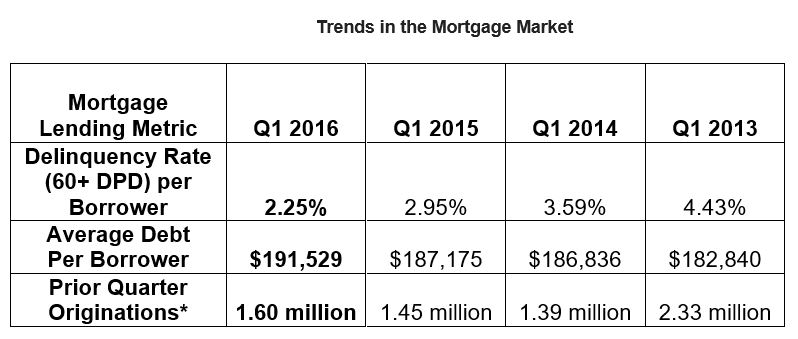

Overall serious delinquency levels in Q1 remained relatively low despite the increases in serious delinquencies in both the auto loan and credit card categories, up to 1.12 percent and 1.47 percent, respectively. The share of serious delinquencies on mortgage loans declined year-over-year by nearly a quarter, from 2.95 percent down to 2.25 percent, according to TransUnion.

While pointing out that the delinquency rates in the auto loan and credit card spaces have been pushed up by an increase of loans to non-prime credit risk borrowers, Ezra Becker, SVP of research and consulting in TransUnion's financial services business unit, said the decline in mortgage delinquencies was due to improvements in the economy and the labor market.

“It's also important to note that mortgage loans and the growing consumer loan space continue to either see declining or muted delinquencies,” Becker said. “This is a result of an economy that is functioning well in terms of consumer credit, with an employment picture that is stronger than it has been in several years.”

“It is heartening to see that, despite concerns that TRID implementation would negatively impact mortgage originations, we still observed growth at the end of 2015.”

Joe Mellman, TransUnion

The serious delinquency rate for mortgages—defined as those 60 or more days past due—has declined now for 10 consecutive quarters and at 2.25 percent, is less than one-third of its peak level of 6.94 percent from the first quarter in 2010.

“It is heartening to see that, despite concerns that TRID implementation would negatively impact mortgage originations, we still observed growth at the end of 2015,” said Joe Mellman, VP and mortgage business leader for TransUnion. “We are well positioned for the spring home buying season, as lenders are more familiar with TRID requirements and strong employment and low interest rates continue.”

Not only are serious delinquencies on mortgages declining, but fewer consumers had mortgages in the first quarter of 2016 (67 million) compared to a year earlier (67.4 million), and mortgage originations (viewed one quarter in arrears to ensure all accounts are included) increased by 10.6 percent year-over-year in Q4 2015, from 1.45 million up to 1.60 million, according to TransUnion.